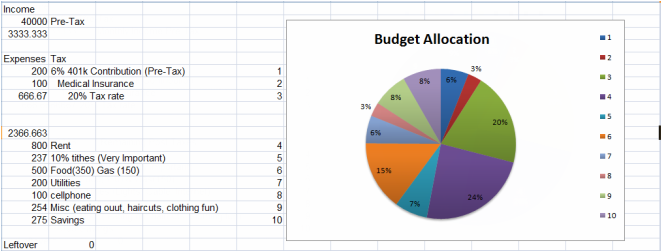

For the past few weeks I have been discussing how to save, ways to reduce spending, and the ideal amount you should spend per category to maximize your effort. This week I will take it a step further and create a mock budget using a few of the tactics. We will start with 40k Pre-tax, the reasoning behind that number is what a recent college graduate can expect to make +/- 5k depending on his/her career choice. $40k is a reasonable amount of money for a new college grad, but we will quickly see how taxes and bills take that money away and leave little room for enjoyment.

As we can see above with a salary of 40k pre-tax, there will be little wiggle room, and some of my estimates are on the conservative side. $800 for rent is around the average price for a 1/1, to help make room in the budget I would suggest getting a roommate and obtaining a 2 bedroom apartment. One MAJOR expense that could not be included in the budget due to lack of funds is student loan payment. You might ask how could I not calculate this into the budget when it’s a major part of post college life. The simple answer, the money simply is not there! This fact can be seen by the number of defaults and late payments made monthly on student loans, the best way to avoid this is keep student loans as low as possible. Overall the budget is not horrible since there is room for savings and contributions to a 401k, and we have to remember this is just the first job, there will be growth in salary to allow for better living. Don't worry!

As we can see above with a salary of 40k pre-tax, there will be little wiggle room, and some of my estimates are on the conservative side. $800 for rent is around the average price for a 1/1, to help make room in the budget I would suggest getting a roommate and obtaining a 2 bedroom apartment. One MAJOR expense that could not be included in the budget due to lack of funds is student loan payment. You might ask how could I not calculate this into the budget when it’s a major part of post college life. The simple answer, the money simply is not there! This fact can be seen by the number of defaults and late payments made monthly on student loans, the best way to avoid this is keep student loans as low as possible. Overall the budget is not horrible since there is room for savings and contributions to a 401k, and we have to remember this is just the first job, there will be growth in salary to allow for better living. Don't worry!

RSS Feed

RSS Feed